On Thursday afternoon, Rep. Bruce Skaug presented House Bill 649 to the House Business Committee, related to so-called predatory lenders. According to the bill’s statement of purpose:

This legislation prohibits usury in lending by non-regulated entities. Regulated entities, such as banks and credit card companies are otherwise regulated. Parties may agree to payment of interest and fees not to exceed 30%, or 10% over the prime rate as published by the federal reserve, whichever is higher.

Idaho Freedom Foundation rated H649 -2, saying that it represents both government regulation of the free market and interference in the right of contract between individuals. Its analysis denied that payday loans are usurious:

Charging any rate of interest that is clearly specified in a contract and voluntarily agreed to by all parties cannot rationally be defined as usury.

Watch the full committee hearing here:

In his presentation, Rep. Skaug explained the history of usury laws in Western civilization. Judaism, Christianity, and even ancient Greece and Rome prohibited moneylenders from charging exorbitant interest. He also shared stories of Idahoans who turned to short-term loans and found themselves in a downward spiral of debt. He characterized the industry as predatory.

Several testifiers agreed, saying the bill was necessary to uphold biblical principles as well as societal cohesion.

The final testifier, and the only one in opposition, was Dennis Bassford, the CEO of MoneyTree, a short-term loan business with a presence in Idaho. Bassford, along with his brother David and sister-in-law Sara, has operated MoneyTree throughout the western United States since 1983. Despite founding the company in Washington, Bassford is an Idaho native who graduated from BSU.

He defended the short-term loan industry before the committee, saying it is often a last resort for those who cannot obtain credit any other way. He said that if Idaho were to impose restrictions such as those in H649, borrowers could be driven to unregulated foreign online lenders.

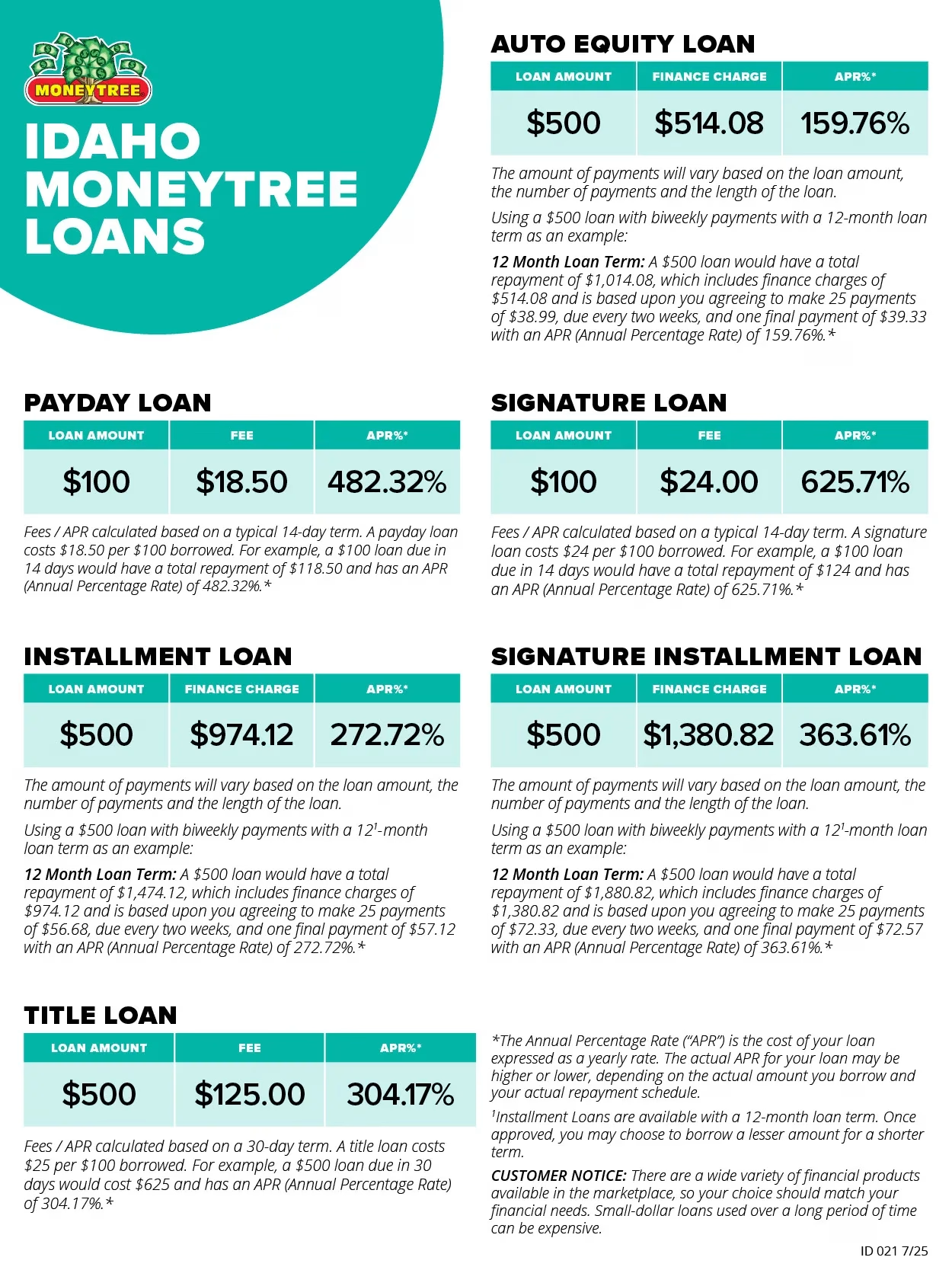

Members of the committee peppered Bassford with questions. He said that the average short-term loan was $300, and that borrowers paid a flat fee of $18.50 on every hundred dollars borrowed. He also said that the average term for loans was 21 days. Committee members did the math, figuring that this would total $55.50 over the course of the three weeks, which works out to an APR of approximately 321%.

Bassford pushed back on that number, saying that what MoneyTree offers are not “APR products.” He explained that the $18.50 per $100 is a flat fee, with no compounding. Rep. Skaug had said that borrowers often roll over loans, taking out new loans to pay off the old ones, but Bassford said that isn’t legal.

More than a decade ago, Washington levied a half-million-dollar fine against MoneyTree for deceptive advertising, false collection letters, and improper access to customer bank accounts. The issue came up in Thursday’s hearing, but Bassford dismissed it.

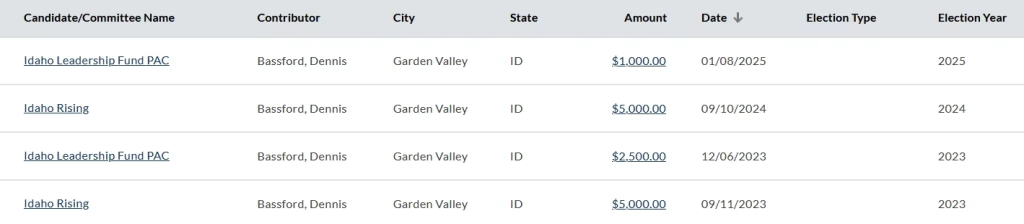

Dennis Bassford and MoneyTree have engaged in political donations and lobbying at the national level, as well as in states such as Washington and Nevada. They have done relatively little in Idaho to this point. According to Sunshine, Bassford has donated four-figure sums to two PACs—Idaho Rising and Idaho Leadership Fund—over the past few election cycles.

House Speaker Mike Moyle chairs Idaho Rising, which supported Republican candidates in 2024 as well as opposing ranked choice voting. Lt. Gov. Scott Bedke is associated with Idaho Leadership Fund, which appears to support moderate Republican candidates.

Despite Bassford’s claim that MoneyTree doesn’t offer “APR products,” the company’s own website displays the equivalent APR for each option:

During debate, Rep. Mike Veile pointed out that the same $300 loan would be capped at about a dollar fifty per week under this bill. That could potentially make the short term lending industry an nonviable business model in Idaho.

Rep. Brent Crane originally moved to send H649 to the floor with a recommendation that it pass, but after some backroom discussion with Rep. Skaug and Chairman Jordan Redman, he withdrew his motion and instead moved to send the bill to the amending order. He suggested that Skaug work with Bassford to figure out a more viable number. The committee agreed.

This is a complicated issue. Usury has long been considered sinful and wrong—remember the villain Shylock in Shakespeare’s The Merchant of Venice—but in recent decades it has become much more accepted in our society. Is a short-term lender who can loan you $300 in cash to tide you over until your next paycheck, at the cost of an extra $55, a necessary part of modern society, or a parasite that exploits vulnerable citizens?

Does government have a role in protecting people from contracts that they ostensibly freely enter into? Pure libertarians would say no—that people have the right to enter into any kind of contract they want, no matter how exploitative it might seem. Is it entirely the responsibility of the individual to decide if an effective APR of 321% is reasonable for their situation?

Or is this something like online gambling, pornography, prostitution, or certain drugs that our society has decided are not acceptable?

H649 is headed to the amending order, where lawmakers could potentially change the 30% cap to something different. After that, it must still pass the House, then head over to the Senate to do it all over again. In the meantime, tell me what you think: Should Idaho set limits on lending?

Feature image created with Microsoft Copilot.

Gem State Chronicle is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

About Brian Almon

Brian Almon is the Editor of the Gem State Chronicle. He also serves as Chairman of the District 14 Republican Party and is a trustee of the Eagle Public Library Board. He lives with his wife and five children in Eagle.